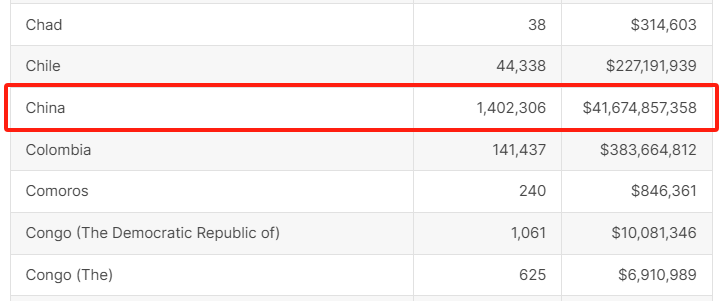

2月10日,澳大利亚税局(Australian Taxation Office, ATO)发布《2024年澳大利亚按司法管辖权交换CRS账户报告》(2024 Australian CRS reportable accounts by jurisdiction)。报告显示,2024年澳大利亚税务机关已经向中国税务机关交换140余万个在澳中国税收居民个人的金融账户,涉及资产总额超过416亿澳元,无论账户数量还是资产规模均位居全球交换国家和地区首位。相较于2023年披露的数据,澳大利亚税务机关向中国税务机关交换的金融账户数量增幅达20%。

我国自2018年9月完成首次CRS信息交换以来,已与全球100多个国家和地区实现了金融账户的数据互通。除CRS框架下的金融账户信息自动交换外,税务机关还可针对具体案件向他国发起专项情报交换以调取涉税证据。在前述制度背景下,取得境外所得的税收居民收入更为透明,面临更为严格的监管态势。2025年以来,已有多地税务机关通报取得境外所得未申报案件,通过“五步工作法”督促相关人员补缴税款;据新华网今年年初报道,“税务机关持续加强对居民个人境外所得纳税的宣传辅导,去年以来提醒纳税人对2022年至2024年从境外取得的收入进行自查”。在全球税收透明化的背景下,高净值等人群应全面梳理境外所得,及时补缴税款,对于政策规定模糊的所得或已经超过追征期的税款等,应与税务机关进行沟通,提交相关证明文件等妥善处理。

Limitations of the CRS report

The Total accounts column represents the number of Financial Accounts held by foreign tax residents; it does not represent the number of foreign tax residents holding accounts. An account holder may be a tax resident of multiple jurisdictions, so accounts may be reported more than once.

The Balance ($A) column represents the total balance or value of the Financial Assets held in the accounts. The figure includes:

● cash

● securities

● bonds

● commodities

● partnership interests

● debt interests and equity interests.

Where an account is held by more than one account holder, the balance or value is attributed in full to each account holder. Where an account is held by a passive non-financial entity, such as a trust, the value of the equity interest is attributed in full to each controlling person. These accounts will be reported in the Total accounts and Balance ($A) columns more than once.

CRS statistics 2024

来源:Australian Taxation Office